Insurance Business unearths a trail of missed opportunities

The insurance industry has been roundly criticised on buildings insurance costs and “secret” commissions paid to property managing agents and freeholders, and a trail of documents show missed opportunities for watchdogs and government to tackle the problem dating as far back as 2005.

Leaseholder representative anger has been compounded by a July exchange between FCA leaders and MPs that took place at a Treasury Sub-Committee hearing to investigate multi-occupancy building insurance and rip-off commissions.

It took a “terrible tragedy and a letter from [Secretary of State for Levelling Up, Housing and Communities] Michael Gove” for the regulator to take action on the leasehold insurance costs issue, it was put to FCA executive director, consumers and competition Sheldon Mills and FCA director of general insurance and conduct specialists Matthew Brewis, by committee chair Harriet Baldwin MP.

In a preceding September 2022 report, one commission payment was as high as 62%, with “most” brokers found to have agreed commissions of more than 30%. In 39% of cases reviewed by the regulator, more than half of the commission was paid by the broker to property managing agents or freeholders. The FCA further found that there was often little evidence provided to show fair value, particularly where freeholders were pocketing sums. The taking of commissions by third parties is a practice that Gove has vowed to ban, to be replaced with a “more transparent” fee model.

“The thing that has struck me most about this consultation is that these absolutely egregious commissions that have surfaced in your market study have been going on under nose of the FCA for, presumably, the entire lifetime of your organisation,” Baldwin quizzed Mills. “Were you also shocked by what you found out about this market?”

The regulator had been made aware of leaseholder complaints on rising insurance costs “just prior” to ministerial communication received in January 2022, Mills responded. The FCA executive director had been “surprised” to see such high commissions, MPs heard.

It is less that the testimony could have suggested that the FCA was recently made aware of issues with leaseholder insurance commissions that has caused frustration; rather, parties told Insurance Business that the comments suggested at best a lack of awareness on an issue that has been raised with it for a decade, and at worst feigned ignorance.

Sir Peter Bottomley MP, Father of the House, told Insurance Business he had been bringing up the “secret” commission issue in Parliament and with the FCA for 10 years. Sir Peter has been in touch with Mills’ office since the July committee hearing, Insurance Business understands.

“The experts, the regulators, the insurance companies all knew of this,” he told Insurance Business. “It was money for old rope for the in-crowd, and it was paying out a fortune unnecessarily for the masses.”

Regulators have been less “blindsided” – as FS Consumer Panel member Johnny Timpson put it when quizzed by the committee – than wearing blinkers, it was alleged by leaseholder advocates. They have argued that a paper trail shows that successive regulators may have scuppered chances to address the issue for nearly two decades.

“The FCA themselves looked at this issue in 2014, and said it was a problem – so for the executive director to say they’d only just heard about it is not credible,” Leasehold Knowledge Partnership chair Martin Boyd said.

The LKP chair described Mills’ comments as “unbelievable”. LKP has written to the regulator to demand a meeting over what it has alleged are factually inaccurate statements.

“The FCA has been appallingly weak on this issue, and they’re still showing a complete unwillingness to act dynamically,” Boyd said.

An FCA spokesperson said: “We have worked quickly to draw up and consult on a package of important reforms that will give leaseholders greater rights and transparency in the multi-occupancy buildings insurance market.

“These rule changes include requiring insurance firms to act in leaseholders’ best interests and banning firms from recommending a policy based on the levels of commission or renumeration. We will act where firms are not following our rules.”

The 2005 FSA investigation

Insurance industry insiders have previously expressed dissatisfaction with the FCA’s handling of the matter and pointed out that successive watchdogs have been made aware of the issue.

“This is a problem that has not just manifested itself in the last one year – this has been around for donkey’s years, this predates the FSA taking over the regulation of general insurance in January 2005,” said Branko Bjelobaba, Branko principal, speaking prior to the committee meeting. The compliance consultant scored the regulator a “three” out of 10 for its performance on secret commissions, citing time taken to tackle the issue.

In 2005, FCA predecessor the Financial Services Authority (FSA) concluded, following a private investigation, the report on which was never made public but was ultimately supplied to LKP with redactions following a freedom of information request, that there was “minimal evidence” of any concern regarding the potential for brokers and property managing agents to be overinflating charges, despite contact from multiple individuals and MPs.

In its report, however, the regulator said it was unable to say “with certainty” that bad practices were not widespread.

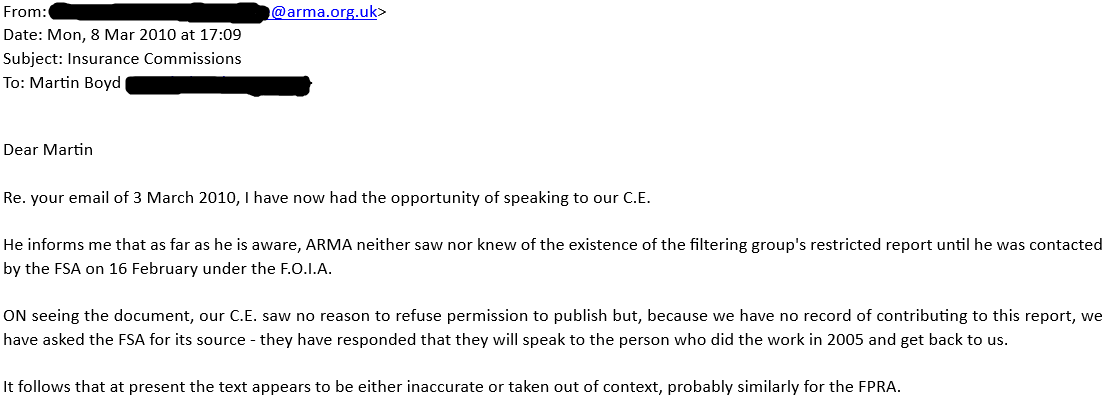

LKP chair Boyd has questioned how deep into the issue the FSA dug. When Boyd reached out to ARMA in 2010, a representative set out that it had “no record” of having contributed to the report despite having been cited in it as an approached organisation, according to emails sent to Boyd and seen by Insurance Business.

“On seeing the document, our C.E. [chief executive] saw no reason to refuse permission to publish but, because we have no record of contributing to this report, we have asked the FSA for its source – they have responded that they will speak to the person who did the work in 2005 and get back to us,” an ARMA representative wrote to Boyd in the 2010 email. “It follows that at present the text appears to be either inaccurate or taken out of context, probably similarly for the FPRA.”

Email exchange between Martin Boyd and an ARMA representative (name redacted) from 2010 – supplied by Leasehold Knowledge Partnership

The Property Institute (TPI) CEO Andrew Bulmer was unable to confirm or deny any ARMA involvement when approached by Insurance Business, citing the passage of time. The current chair and vice chair at FPRA were also unable to corroborate participation in the investigation, though they too were not in post at the time.

Despite the issue having been raised by multiple MPs and posing a potential reputational issue for the regulator, according to its own 2005 report, by 2009 no action had been taken on the buildings commissions issue – though a media report shows it continued to be raised with the FSA.

FCA flagged the leasehold commission issue in 2014 – but did not tackle it

In 2013, the FCA was formed and took over oversight of general insurance from the FSA. A year later, the Competition and Markets Authority (CMA) published its 2014 residential property management services market study, in which broker buildings insurance commissions were again flagged, among a ream of other potential harms.

The CMA document cited evidence from an FCA market impact report on wider commercial insurance practices from that same year that showed both insurers and brokers had raised concerns around the risk of leaseholders facing inflated charges.

“Some of the intermediaries and insurers we spoke to expressed concerns that these commission rates exist because the customer buying the insurance product was not the business or individual ultimately bearing the cost of the product,” the FCA’s 2014 reported stated. “This appears to result in some intermediaries and property owners sharing in high commission levels with the inflated costs (and any potential detriment) being borne by the underlying tenant or lessor.”

The CMA recommended “consideration of the appropriate coverage of regulation in this case by the FCA and by government more generally”, having found that it would be “extremely challenging” for leaseholders to determine whether they were paying excessive costs.

Following its thematic review, which led to a fine of over £4 million against small and medium enterprise (SME) specialist broker Bluefin (then owned by AXA) over inadequate systems and controls, the FCA did take some measures to tighten up insurance broking controls more broadly, including work around disclosure. However, as leaseholders were not defined as customers, such advancements had a limited impact for them.

Grenfell Tower fire brings insurance costs under the spotlight

It took the tragic 2017 Grenfell Tower fire, which saw 72 dead and a raft of costly fire remediation and safety measures – including waking watches – in its aftermath, to thrust insurance cost issues back into the public gaze and, in the years to come, the regulatory spotlight.

The regulator engaged in discovery work as insurance premiums soared and insurers shied away from the market in the years that followed the blaze. The FCA’s efforts included collating and analysing correspondence received, in addition to engaging with trade bodies, industry and other agencies and an All-Party Parliamentary Group, Insurance Business understands.

Years on from Grenfell, fire instances were down and combustible cladding had been removed from 85% of at-risk high-rises.

Nevertheless, “dramatically” increasing premiums and a lack of insurers willing to offer cover spurred Gove to call for regulatory action.

In his January 2022 letter to the regulator, Gove demanded “urgent advice” and wrote of concerns that despite remediation changes, premiums continued to increase for many.

“The market lacks transparency and there is not currently useful data to explain the rationale behind the increasing premiums charged by insurers and the conditions associated with the cover,” the minister said. “The role and remuneration of brokers, managing agents and freeholders is also unclear.”

It was following Gove’s demand that the FCA again publicly broached the leasehold insurance topic, against a backdrop of media outcry – including a high-profile Jeremy Clarkson op ed in The Times – and ministerial scrutiny. The regulator produced two reports investigating the market and went on to release a raft of proposals.

“It took the leaseholders three years to get a decision from the lowest tribunal in the land, the first-tier tribunal, and it only happened because of a formidable leaseholder that is retired, that is a magistrate judge and has an accounting background,” said Commonhold Now co-founder Harry Scoffin.

Other leaseholders had been powerless to act, advocates said, with the value of many leasehold properties deteriorating amid soaring charges and insurance costs.

“A lot of leaseholders have not got accounting, or legal, or insurance backgrounds, so it is like trying to find a needle in a haystack,” Scoffin said.

That the FCA has now acted has been welcomed to some degree, and should offer some relief to those affected, though stakeholders have contended that changes do not go far enough, and there are further issues driving up insurance costs that have compounded problems in recent years. That the insurance commission issue itself was an “unexploded bomb”, to quote Baldwin, that was lurking out of the regulator and others’ line of sight is a tough pill that many will not swallow.

Related Stories

Keep up with the latest news and events

Join our mailing list, it’s free!

This page requires JavaScript