Insurance Business lists the essential kinds of insurance small businesses need in this article. If you own a small enterprise and are trying to work out which policies suit your needs, this piece can serve as a useful guide. If you are one of the many insurance professionals who visit our site, this article can serve as a perfect guide for clients who have questions about insurance for small businesses.

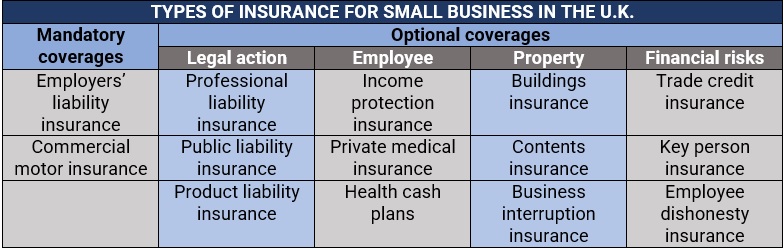

There are two types of insurance policies that small businesses are legally required to have, according to the Association of British Insurers (ABI). These are:

- Employers’ liability insurance – which is mandatory for all businesses with at least one employee.

- Commercial motor insurance – which is compulsory for those that operate a vehicle for business purposes.

The rest are optional coverages that small businesses can access depending on their specific needs. The ABI grouped these discretionary insurance policies into four:

- Protection against the risk of compensation claims and legal action

- Protection against the risks to your property

- Protection against the risks your employees face

- Protection against financial risks

We will discuss these policies, along with the compulsory coverages, in detail below.

Mandatory insurance for small businesses

Most businesses in the UK are legally required to take out these policies. Getting caught operating without one comes with serious penalties.

1. Employees’ liability insurance

If your business employs at least one staff, the law requires you to take out employers’ liability insurance. Also called EL insurance, this type of coverage works just like workers’ compensation policies in other countries, providing financial protection if your employee gets sick or injured while performing their jobs. You need to purchase coverage for these members of your labour pool:

- Full-time workers

- Part-time workers

- Staff on casual employment

- Volunteers, if you operate a non-profit

EL insurance typically pays for:

- Medical and treatment expenses

- Loss of income

- Legal costs

The law also requires that you purchase employers’ liability insurance only from authorised insurers or specialist brokers through the British Insurance Brokers’ Association (BIBA). Coverage must be at least £5 million, although most insurers offer a minimum protection of £10 million.

If your business is caught operating without EL insurance, the Health and Safety Executive (HSE) can impose a £2,500 penalty for each day you go uninsured. You can likewise be fined £1,000 if you fail to display your employer’s liability certificate, or for any reason, refuse to show it to inspectors when asked.

Businesses without employees or those operated exclusively by families, meanwhile, are not mandated to take out EL insurance.

2. Commercial motor insurance

Standard car insurance does not cover business-use vehicles, so if your company operates one, you need to purchase commercial motor insurance. This type of specialist policy operates under the same principle as private motor insurance, paying out for bodily injury and property damage that you have caused, and depending on the level of cover, can include repair and replacement costs of the insured vehicle.

Commercial motor insurance is actually an umbrella term for all types of coverage that businesses operating commercial vehicles can access. These are:

- Third-party coverage: The minimum requirement to be able to operate a commercial vehicle, this pays out for costs incurred due to injury or damage to other people’s property because of an accident involving your car.

- Third party, fire & theft (TPFT) coverage: In addition to third-party injury and property damage, this covers your commercial vehicle if it is stolen or destroyed in a fire.

- Comprehensive coverage: Provides financial protection against anything covered by third-party and TPFT policies, as well as additional coverages, including damage your vehicle sustains, regardless of who is at-fault.

Specialist motor insurance policies are also available if commercial vehicles form a core part of your business. These include:

- HGV insurance

- Taxi fleet insurance

- Truck insurance

- Van insurance

Insurance for small businesses covering compensation claims and legal action

These types of insurance policies for small businesses cover your legal liabilities towards the general public, including your clients.

1. Professional indemnity insurance

Professional indemnity insurance, also referred to as PI insurance, is designed for businesses offering professional services or advice. These include:

- Advertising professionals

- Accountants

- Architects

- Business consultants

- Chartered surveyors

- Financial advisers

- Healthcare professionals

- Interior designers

- IT service providers

- Programmers

- Public relations professionals

- Publishers

- Recruitment consultants

- Solicitors

If you operate these types of businesses, professional indemnity coverage can protect you from claims arising from negligent acts or omissions committed while providing services. PI insurance covers legal and compensation costs. Although not legally required, some clients may insist that you take out coverage before doing business with you.

Are you interested to learn more about this form of protection? Then check out this comprehensive guide, where we answer all your questions regarding professional indemnity insurance.

2. Public liability insurance

Public liability insurance, also called PL or general liability insurance, protects your business from claims of property damage or bodily injury resulting from actual or alleged negligence in your business activities. Because of the level of coverage it provides, PL policies have become among the most popular insurance for small businesses in the UK.

Similar to professional indemnity insurance, some customers may request that you purchase public liability insurance as a condition for working with them.

3. Product liability insurance

Product liability insurance protects your business if someone suffers an injury or property damage due to the use of a faulty product that you design, supply, or manufacture. This type of policy pays out for legal and compensation costs.

Even if your business was not involved in the manufacture of the defective product, you may be held liable if:

- Your business’ name is indicated on the product

- Your business was involved in repairing, refurbishing, or changing the product

- You imported the product outside the European Union

- You cannot identify who manufactured the product

- The manufacturer of the product has gone out of business

Ideally, businesses should purchase a product liability insurance policy that pays out between £1 million to £5 million in compensation costs.

Insurance for small businesses providing commercial property protection

These types of insurance for small businesses are designed to minimise the disruption to your business’ day-to-day operations by providing compensation for damages and losses caused by a covered peril.

- Buildings insurance: Pays out for losses or damages that happen to the property or building your business operates in.

- Contents insurance: Covers the cost to repair or replace physical belongings vital to your daily operations, including laptops, smartphones, and other mobile devices. It also covers damages or losses caused by fire, vandalism, theft, flooding, and other insured events.

- Business interruption insurance: Also called BI insurance, this protects your business from loss of income and additional costs incurred if you are forced to shut down operations due to an unexpected event.

The disruption brought about by the COVID-19 pandemic has given prominence to this type of coverage. You can check out our coverage highlight to learn more about how the latest issues surrounding business interruption insurance impact your operations.

Insurance for small businesses designed to protect your employees

These types of policies, along with employers’ liability insurance, help provide medical assistance and financial security for your business’ most valuable assets – your employees.

- Income protection insurance: Provides a monthly payout that serves as a replacement for an employee’s income if they are unable to work due to a medical condition, including illnesses and injuries.

- Private medical insurance: Covers the cost of private medical care, allowing your employees to receive treatment faster, minimising disruption to your operations.

- Health cash plans: Reimburses a portion or the entire cost of routine or unexpected healthcare procedures, including visits to dentists, opticians, or physiotherapists.

Dental care is among the typical inclusions in a health care plan. If you want to know how dental insurance works across the country, you can check out our comprehensive guide on dental insurance in the UK.

Insurance for small businesses designed to protect against financial risks

These insurance products provide your business with some form of financial safety net against bad debts and unscrupulous employees.

- Trade credit insurance: Provides financial cushion if customers fail to pay or are late in paying for products or services your business renders.

- Key person insurance: Provides financial benefit to your business if a vital team member becomes disabled or dies. The payout is intended as monetary support as your enterprise goes through a transition period to find and train a replacement.

- Money insurance: Covers money stolen from your business, whether it happens within your premises or while in transit.

- Employee dishonesty insurance: Protects your business against workers who steal money or stock.

Here’s a summary of the different types of insurance policies that are worth considering for small businesses in the UK.

Choosing which small business insurance policies suit your needs can be a complicated endeavour given your numerous options. An experienced insurance agent or broker can help you filter through the noise and guide you in finding the right coverage for your business.

Compared to their larger counterparts, small businesses operate on limited financial resources, making them extremely vulnerable should major losses occur. The latest figures from GOV.UK revealed that the country’s business population continued to decrease, sliding down by about 7% or about 472,000 businesses, since the height of the pandemic in 2020.

These figures highlight the need for businesses to be financially protected, especially the smaller ones, which form the backbone of the UK’s economy. GOV.UK’s data also showed that small businesses, or those with less than 50 employees, comprise 99.2% of the UK’s 5.5 million-strong private sector operations.

This backbone, however, is facing a tremendous protection gap, with just slightly over a quarter, or 26%, carrying some form of coverage, according to a recent poll conducted by industry giant AXA UK. The survey, which involves 500 micro-businesses or those employing fewer than nine personnel, also reveals that only 40% of owners have additional personal savings that can serve as a safety net in case their business gets into financial difficulty.

As AXA UK’s survey suggests, it is possible to operate a small business in the UK without insurance. The question is are you willing to take that risk? If your business does not have employees and a company vehicle, you can do away with your employer’s liability and commercial motor policies – the only mandatory coverages for businesses in the country.

But should an unfortunate event happen – theft, natural calamity, or lawsuit, for example, without any form of financial protection, these events can run your operations into the ground. So, while it is technically possible to go about with no proper coverage, experts still advise that you take out insurance for small businesses to be protected from unexpected disasters.

Because each small business’ coverage needs vary significantly, it is difficult to come up with a one-size-fits-all figure to represent how much insurance for small businesses costs in the UK. Insurers consider a range of factors when calculating how much your premiums will be priced. These include:

- The nature of your small business

- The industry your business is in

- The number of your employees

- The types of small business insurance policies you are taking out

- Your coverage amount

- The excess amount

- Your business’ claims history

Each insurer calculates premiums differently. If you want to find out how they do, you can check out our comprehensive guide to insurance premiums.

If you’re self-employed and don’t have anybody else working for you, then you can skip employer’s liability insurance. The same with commercial motor insurance if you do not use a vehicle to run your business.

Other types of insurance for small businesses, however, may prove useful. If you offer professional advice or service, then professional indemnity insurance can help protect you financially from claims of losses that resulted from the services you rendered. Public liability insurance, meanwhile, can cover you if someone gets injured or had their personal belongings damaged because of your business activities.

Another thing to take note of is that as a self-employed individual, you should be able to claim your business insurance costs as an allowable expense to minimise your taxes.

Depending on the type of home business you run, there are certain types of insurance for small businesses that are worth taking out. Professional indemnity insurance suits your business if it offers professional services as this type of coverage provides financial protection if you get sued because of the services you render.

You can also consider purchasing business contents insurance as the equipment you use for your business – such as laptops and other office supplies – are not often covered by your standard home insurance policy.

Of course, there’s employers’ liability insurance that you are required to purchase if you have staff working for you and commercial motor insurance if you use your vehicle for business purposes.

If you’re in the construction business, meanwhile, there are certain types of insurance policies that you need to take out to keep you financially protected. Find out what these are in our construction insurance guide for UK builders.

Can you think of other types of insurance for small businesses that we might have missed? Key in your thoughts in the comment box below.